How to Get Your Money Back After Being Scammed: A 2026 Guide

Discover the exact steps to take after being scammed to maximize your chances of getting money back, by payment method, urgency window, and reporting agency. Includes bank reversals, crypto recovery options, FTC claims, and how Truvizy prevents future losses.

· By Truvizy Research Team · 8 min read

TL;DR

Getting money back after a scam is possible in a minority of cases, fewer than 5% of victims recover full losses according to the FTC. Speed is everything: report within 24 hours to your bank, card issuer, or crypto exchange. File with FBI IC3 and the FTC for any amount. Credit cards offer the highest chargeback success rate; cryptocurrency is the hardest. Truvizy helps detect scams before any money is sent.

You send $2,400 to what appears to be a PayPal overpayment refund from a private buyer. You follow their instructions, forward the difference to a "shipping agent," and within the hour you realize the original payment notification was fraudulent. The money is gone. Your first question, almost everyone's first question in this situation, is whether you can get it back. The honest answer depends on how fast you act, how you paid, and which agencies you contact within the critical first 24 hours.

What "Getting Money Back" After a Scam Actually Means

Recovery from a scam is not a single process, it is a different set of procedures depending on the payment method used, the amount lost, and how quickly you report. "Getting your money back" covers at least four distinct mechanisms: bank chargebacks, regulatory consumer protection claims, law enforcement recovery actions, and private legal remedies. Each has a different timeline, success rate, and minimum threshold.

Credit card chargebacks and bank disputes offer the highest success rates because the financial system has built-in consumer protections for unauthorized or fraudulent transactions. Wire transfers and bank-to-bank payments are significantly harder to reverse because they settle quickly and often cross international borders. Cryptocurrency is the hardest: transactions are irreversible by design, and meaningful recovery requires law enforcement intervention or the receiving exchange voluntarily freezing assets.

Understanding this landscape before you call your bank prevents wasted time and missed deadlines. Each payment type has a specific legal window, and missing that window can permanently eliminate your options for a chargeback or reversal under federal consumer protection law.

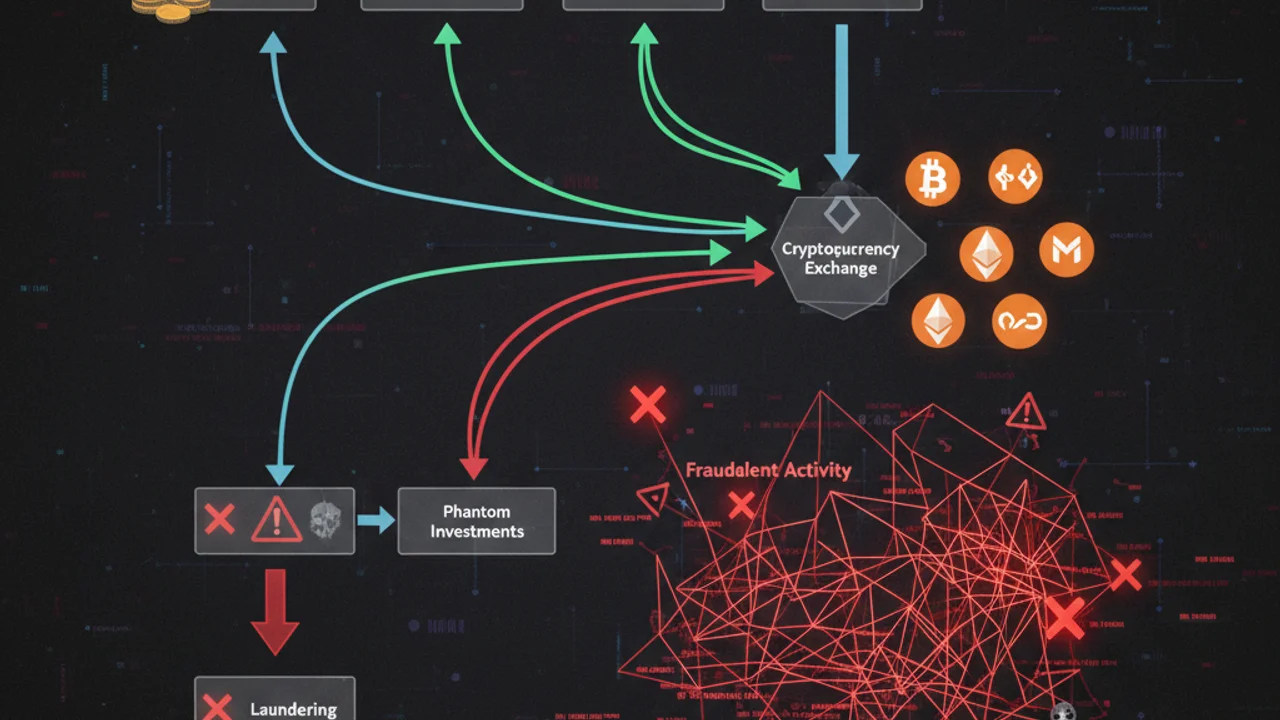

How Scammers Move Money to Make Recovery Difficult

Professional fraud operations are explicitly designed to defeat recovery mechanisms. Understanding their methods helps you identify which steps still have a chance. According to the FBI IC3's 2024 Annual Report, scammers move stolen funds through a predictable sequence that completes between 10 minutes and 48 hours after the initial transfer.

Layer 1, Mule accounts. Funds land first in a money mule account, a real bank account held by a recruited third party, often themselves a victim of a separate job scam. This creates distance between the initial transaction and the scammer's own accounts, complicating tracing for banks and law enforcement.

Layer 2, Rapid conversion. Funds are immediately converted to cryptocurrency or wire-transferred internationally. Once outside the domestic banking system, chargeback protections no longer apply. According to FinCEN, most scam proceeds reach international accounts within 24 hours of the initial transfer, which is why speed is the single most important variable in any recovery attempt.

Layer 3, Cryptocurrency mixing. High-value fraud operations run proceeds through mixing services that obscure transaction trails. This does not make recovery impossible, but it requires blockchain forensics capabilities available only to specialized law enforcement units and private analytics firms, not to individual victims or standard bank fraud teams.

Immediate Steps by Payment Method

Your recovery options and the urgency of each action depend entirely on how you sent money to the scammer. Take these steps now, not tomorrow morning.

Credit card: Call your card issuer immediately to report fraud and initiate a chargeback. Under the Fair Credit Billing Act (FCBA), you have 60 days from the statement date to dispute a charge. Chargebacks on credit cards succeed in roughly 60% of reported fraud cases when filed within the deadline, according to the Consumer Financial Protection Bureau. Document exactly what you were promised versus what you received, this is your chargeback evidence.

Debit card or bank transfer: Call your bank's fraud line now, not in the morning. Under Regulation E, you must report unauthorized debit card transactions within 60 days to maintain full liability protection. For bank-to-bank wire transfers, a bank may be able to recall the transfer if the destination account has not yet forwarded the funds, but this window is typically 24 hours or less. Ask your bank specifically to file a SWIFT recall request if it was an international wire.

Zelle, Venmo, CashApp: Peer-to-peer platforms offer minimal fraud protection for "authorized" transactions, when you sent money willingly, even if deceived. Despite Congressional pressure, most P2P platforms do not reverse transfers based on scam claims. However, report the fraud to the platform, as repeated reports against the same account can trigger account freezes and protect future victims. File with the FTC at reportfraud.ftc.gov. Your issuing bank may have a separate scam reimbursement policy, ask specifically.

Cryptocurrency: Contact your exchange immediately, Coinbase, Binance, Kraken, and major exchanges have fraud response teams. Provide the destination wallet address and transaction hash. If the funds remain in a hosted exchange wallet and have not moved to a private wallet, the exchange may freeze the destination account. Report to FBI IC3 at ic3.gov with all wallet addresses and transaction hashes. For losses exceeding $10,000, consult a blockchain analytics firm, several specialize in tracing and freezing scam proceeds through coordinated legal action.

Gift cards: Call the card issuer immediately using the number on the back of the card. Major issuers, including Google Play, Apple, and Amazon, have fraud teams that can freeze unused balances. Scammers drain gift card balances within minutes of receiving codes, so act within hours of discovering the fraud. File with the FTC after calling the issuer.

Scan any suspicious video, link, or profile before sending money, Truvizy's AI-powered detection catches scams before they cost you.

How Truvizy Helps You Avoid Losing Money to Scams

The most reliable form of scam "recovery" is detection before any money changes hands. Truvizy's AI-powered multi-layer analysis examines videos, links, and digital profiles to identify fraud signals that are invisible to the naked eye, synthetic media manipulation, AI-generated voice patterns, fabricated testimonials, and known scam operation signatures. When Truvizy flags content as suspicious, it is preventing the loss rather than attempting to reverse it after the fact.

At truvizy.app, users scan investment videos, recruitment content, and suspicious links before engaging. Truvizy's detection is particularly effective against the video-based investment scams and AI voice cloning operations responsible for the largest per-victim losses in the FTC's 2025 dataset, categories where standard reverse image search tools fail because the fraudulent content is custom-generated. Early detection through Truvizy eliminates recovery complexity entirely by stopping the transaction before it occurs.

Where to Report a Scam for the Best Recovery Chance

Filing official reports is not just a civic duty, it directly increases your personal recovery odds. Many banks and exchanges require an official complaint number before opening a recovery investigation. These are the key agencies and what each one does with your report:

According to the FTC's own consumer data, victims who file reports within 24 hours of a scam are statistically more likely to receive partial financial remedies from their banks, because the report provides documented evidence of fraud that dispute processes require. As covered in our guide to reporting online scams, the most common mistake is waiting days before filing, by which time the 24-hour bank recall window has closed and chargeback deadlines are narrowing.

Key Takeaways

- Act within 24 hours, bank wire recalls and exchange wallet freezes are only viable in this window.

- Credit card chargebacks offer the highest recovery rate under FCBA protections; cryptocurrency is the hardest to recover.

- File with the FTC (reportfraud.ftc.gov) and FBI IC3 (ic3.gov) immediately, official complaint numbers unlock bank investigation processes.

- Avoid upfront-fee "recovery services", they are a second scam specifically targeting prior victims.

Expert analysis note: The economics of scam recovery are stark: professional fraud operations are engineered to defeat every domestic recovery mechanism within hours of a transaction. The combination of mule account layering, immediate cryptocurrency conversion, and cross-border transfer routing means that for the majority of victims, prevention remains the only reliable protection. Truvizy's approach, AI-powered detection before financial engagement, addresses the point of maximum leverage in the fraud cycle. As scammers increasingly deploy synthetic media and AI-generated content to legitimize their operations, multi-layer detection that goes beyond URL verification has become the effective standard for consumer protection in 2026.

You sent $3,000 via bank wire this morning to someone you met online, and you now believe it was a scam. What is your MOST time-sensitive action?

- File a report with the FTC, this automatically reverses the wire transfer

- Call your bank immediately to request a wire recall before the funds are forwarded

- Contact an attorney, only legal action can recover wire transfer funds

- Wait to see if the person contacts you again with an explanation

Answer: Wire recalls must be initiated within hours, banks typically have a 24-hour window before funds are forwarded internationally. Call your bank's fraud line now, provide the wire details, and specifically request a 'wire recall.' File with FBI IC3 at ic3.gov and FTC at reportfraud.ftc.gov simultaneously to create a paper trail.

Related reading: How to Report an Online Scam — Step-by-step guide to filing effective FBI IC3, FTC, and platform reports

Related reading: Social Engineering Attacks Explained — How scammers use psychological manipulation to bypass your skepticism

Related reading: Telegram Task Scams — How easy money job scams steal thousands through cryptocurrency deposit traps

Frequently Asked Questions

Can you actually get your money back after being scammed?

Recovery is possible but uncommon, the FTC estimates fewer than 5% of scam victims recover their full losses. Your best chance requires immediate action: report to your bank within 24 hours, dispute the transaction before it settles, and file with FBI IC3 and the FTC the same day. Credit card disputes succeed more often than wire transfers or cryptocurrency.

How do I get a bank refund after being scammed?

Call your bank's fraud department immediately, use the number on your card, not any contact from the scammer. File a written dispute within 60 days of the transaction appearing on your statement. For credit cards, the Fair Credit Billing Act (FCBA) provides chargeback rights. For debit cards, Regulation E applies with a 60-day reporting window to maintain full liability protection.

Is it possible to recover cryptocurrency sent to a scammer?

Cryptocurrency transactions are generally irreversible once confirmed on the blockchain. However, reporting to your exchange immediately, within 24 hours, can sometimes result in destination wallet freezes if funds remain in a hosted wallet. FBI IC3 and specialist blockchain analytics firms occasionally trace and freeze assets for large losses. Success rates are estimated at 3-5% by blockchain forensics firm Chainalysis.

Can Truvizy help me recover money from a scam?

Truvizy does not recover funds directly. Truvizy's AI-powered detection helps you identify scams before you send money, the most reliable form of prevention. Scan any suspicious video, link, or profile at truvizy.app. Truvizy's multi-layer analysis flags fraud signals invisible to standard tools, stopping the loss before it happens rather than attempting recovery after.

What is the fastest way to report a scam in the US?

File with the FTC at reportfraud.ftc.gov (takes 5 minutes) and the FBI IC3 at ic3.gov for online fraud. Call your bank fraud line immediately, most operate 24/7. For investment or crypto fraud, also report to the SEC at sec.gov/tcr and CFTC at cftc.gov/complaint. Filing quickly raises both your personal recovery chances and the likelihood of a criminal investigation.