Zelle and Venmo Scams in 2026: Why Your Bank Will Not Refund You

Zelle and Venmo scams cost Americans over $870M in 2024, and most victims never get refunded. Learn the 7 most common payment app scams and how to protect yourself before sending money.

· Truvizy Research Team · 8 min read

TL;DR

Zelle and Venmo scams are designed to bypass bank fraud protection. Because you "authorize" the transfer, your bank usually treats the loss as your fault, even if you were tricked. The 7 most common variants include fake purchase scams, impostor calls, accidental overpayment, romance bait, rental deposits, prize claims, and "test transfer" tricks. Verify every recipient, never send money to anyone you have not met in person, and use credit cards for purchases instead.

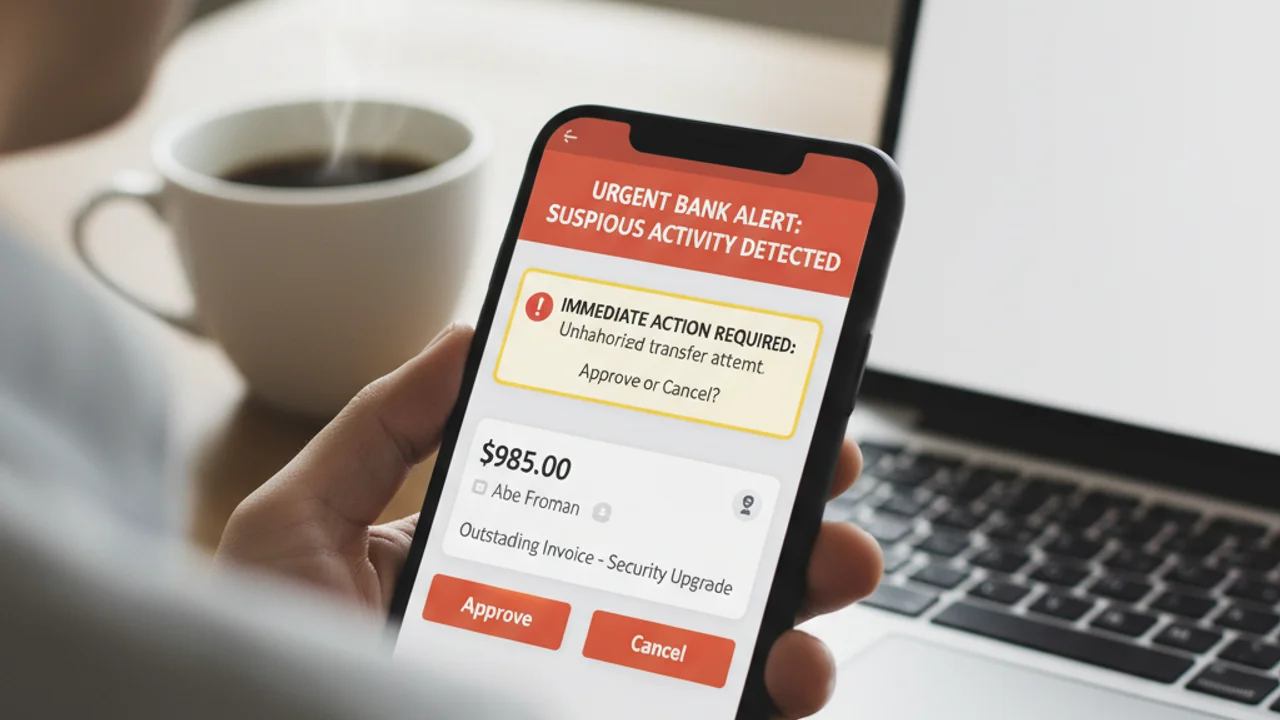

At 9:47 p.m. on a Tuesday, your phone rings with a call from what looks like your bank's fraud line. The voice on the other end says someone is trying to drain your checking account, and the only way to stop it is to send the funds to a "secure recovery account" using Zelle, right now. You do it. Twenty minutes later, the real bank tells you no such recovery account exists, the money is gone, and because you authorized the transfer yourself, you are unlikely to ever see it again. This exact scam, multiplied across hundreds of variations, is why Zelle and Venmo fraud now exceeds $870 million per year in the United States alone.

Quick Answer

What Makes Zelle and Venmo Scams Different

Credit card fraud is reversible. Federal law caps your liability at $50, and chargebacks let you dispute charges directly with the issuer. Zelle and Venmo do not work that way. These peer-to-peer (P2P) services were designed to mimic cash: instant, irreversible, and final. When you press send, the funds move from your bank account to the recipient's in seconds, and the platform considers the transaction complete.

That design choice is exactly what makes Zelle scams so devastating. According to the 2023 Senate Permanent Subcommittee on Investigations report, the four largest U.S. banks (JPMorgan Chase, Bank of America, Wells Fargo, and U.S. Bank) reimbursed only 35% of customers who reported Zelle impostor scams between 2021 and 2022. The Consumer Financial Protection Bureau's 2025 rule expanded refund obligations for some impostor scams, but most fraud categories remain outside Regulation E protection because the user technically authorized the transfer.

How Zelle and Venmo Scams Work

Despite the variety of stories scammers tell, the mechanics collapse into seven core patterns. Recognizing the structure is more valuable than memorizing the cover story, because the cover stories rotate weekly while the structure stays the same.

Red Flags to Spot Payment App Scams

Even one of these signals warrants a pause. Two or more together means you are looking at a scam.

Got a suspicious payment request, screenshot, or link? Scan it on Truvizy before you send a dollar.

How Truvizy Detects Payment App Scams

Truvizy's AI-powered detection works on the artifacts that surround payment app fraud, not the transfer itself. When a romance scammer sends a tearful video begging for emergency Venmo funds, Truvizy's multi-layer analysis flags the synthetic generation signals. When a fake landlord shares photos of an apartment "they own," Truvizy can compare them against known reverse-image hits. When a smishing text from "Zelle Security" links to a phishing page, Truvizy's URL reputation engine can flag the destination before you tap submit.

This matters because by the time you have the recipient details in your Zelle app, you are seconds from an irreversible transfer. The defense has to happen earlier, on the message, the screenshot, the dating profile, the listing photo, the impostor video. Submit any of those at truvizy.app and you get a verdict in seconds, before the money is gone.

What to Do If You Were Scammed

Speed and documentation are everything. Even if recovery odds are slim, you raise them dramatically by acting in the first 24 hours.

Contact your bank immediately and request a Regulation E investigation in writing. Even though most authorized-transfer scams fall outside Regulation E, force the bank to document the denial. The 2023 Senate PSI report found that customers who escalated to written disputes recovered funds 41% of the time, versus 9% for phone-only complaints.

File a complaint with the CFPB at consumerfinance.gov/complaint. The Consumer Financial Protection Bureau directly contacts the bank on your behalf and tracks response patterns. Banks are required to respond, and the regulatory pressure has measurably increased reimbursement rates since 2024.

Report to the FTC and FBI. File at reportfraud.ftc.gov and ic3.gov. These reports feed directly into investigative databases used by the Department of Justice and state attorneys general. Include screenshots, recipient usernames, transaction IDs, and any communication.

Report to the platform itself. In Zelle, report inside your bank app under "Report a Problem." For Venmo, use the in-app report function and Venmo Customer Support. While neither typically reverses authorized transfers, reports help freeze recipient accounts and can help future victims.

If a "bank" call started the scam, file with the FCC at consumercomplaints.fcc.gov. Caller ID spoofing is a federal crime, and FCC enforcement has secured multi-million-dollar penalties against spoofing operations targeting payment-app users.

Key Takeaways

- Zelle and Venmo are designed like cash: once you press send, the money is gone, even if you were tricked.

- Banks deny 65% of Zelle scam reimbursement claims because the transfer is technically "authorized."

- Never send money to a stranger, refund an "accidental" overpayment, or trust a caller who pressures you to move funds.

- If scammed, file written complaints with your bank, the CFPB, the FTC, the FBI IC3, and the platform within 24 hours.

Expert analysis note: Payment-app fraud is now the highest-velocity scam category tracked in the FTC Consumer Sentinel database, growing 4x faster than email phishing and 7x faster than mail fraud. The legal architecture that made Zelle and Venmo possible (instant, peer-to-peer, irreversible) is the same architecture criminals weaponize. Truvizy's position in this stack is preventive: scan the social-engineering artifact before you ever open the payment app.

Your phone rings, the caller ID shows your bank, and the agent says hackers are draining your account but you can save the funds by Zelle-ing $4,000 to a 'secure vault account.' What is the right move?

- Send the Zelle quickly so the bank can rescue the money

- Hang up, call the number on the back of your debit card, and verify the situation with the real bank

- Stay on the line and ask the agent to give you their employee ID for verification

- Send a smaller test Zelle of $100 first to make sure the agent is legitimate

Answer: Real banks never ask you to Zelle yourself or move funds to a 'vault' or 'recovery' account. Caller ID spoofing makes the incoming number look real. The only safe verification is to hang up and call the number on the back of your card. Even one Zelle transfer to the scammer ends the protection: the funds are irreversible the moment you press send.

Frequently Asked Questions

Can I get my money back from a Zelle or Venmo scam?

Usually no. Because you authorized the payment, banks typically classify it as user error rather than fraud. After a 2023 Senate report, Zelle began reimbursing victims of impostor scams, and the CFPB rule that took effect in 2025 expanded protections. Still, only about 1 in 4 victims receives full reimbursement. Report immediately to your bank, the FTC at reportfraud.ftc.gov, and your state attorney general.

Why won't my bank refund a Zelle scam?

Under Regulation E, banks must refund unauthorized transfers, but Zelle scams are usually classified as authorized because you initiated them. The bank treats you as the responsible party even if you were deceived. The 2023 Senate Permanent Subcommittee on Investigations report found that the four largest U.S. banks denied 65% of Zelle scam reimbursement claims. Always dispute in writing and escalate to the CFPB at consumerfinance.gov if denied.

What are the most common Zelle and Venmo scams in 2026?

The seven most reported variants in the FTC Consumer Sentinel database are: fake marketplace purchases (buying goods that never ship), impostor bank calls claiming "fraud protection" transfers, accidental overpayment refund requests, romance and dating app pre-meeting transfers, rental deposit scams, prize and giveaway claim fees, and the "send a test payment" trick used by job recruitment scammers.

Can Truvizy detect Zelle and Venmo payment scams?

Truvizy's AI-powered analysis at truvizy.app scans suspicious links, screenshots, profiles, and videos that scammers use to set up payment app fraud, including fake bank alert texts, fraudulent rental listings, romance scammer profiles, and impostor support call recordings. Submit any suspicious content before sending money to verify whether you are dealing with a known fraud pattern.

Is Zelle or Venmo safer to use?

Neither is "safe" for transactions with strangers. Both treat authorized transfers as final and reversible only at the receiver's discretion. Venmo offers Purchase Protection on payments tagged as "goods or services" for a 1.9% fee, which gives you some recourse. Zelle has no equivalent feature. For any purchase from someone you do not know personally, use a credit card with chargeback rights instead.

Scan a suspicious link or screenshot at truvizy.app — Get an instant safety verdict on the message, profile, or listing before you send any money

How to Spot a Fake Online Store: 9 Warning Signs — The marketplace and seller patterns that lead to Zelle and Venmo purchase scams

How to Get Your Money Back After Being Scammed — The 24-hour recovery playbook that maximizes your reimbursement odds

FAQ

Can I get my money back from a Zelle or Venmo scam?

Usually no. Because you authorized the payment, banks typically classify it as user error rather than fraud. After a 2023 Senate report, Zelle began reimbursing victims of impostor scams, and the CFPB rule that took effect in 2025 expanded protections. Still, only about 1 in 4 victims receives full reimbursement. Report immediately to your bank, the FTC at reportfraud.ftc.gov, and your state attorney general.

Why won't my bank refund a Zelle scam?

Under Regulation E, banks must refund unauthorized transfers, but Zelle scams are usually classified as authorized because you initiated them. The bank treats you as the responsible party even if you were deceived. The 2023 Senate Permanent Subcommittee on Investigations report found that the four largest U.S. banks denied 65% of Zelle scam reimbursement claims. Always dispute in writing and escalate to the CFPB at consumerfinance.gov if denied.

What are the most common Zelle and Venmo scams in 2026?

The seven most reported variants in the FTC Consumer Sentinel database are: fake marketplace purchases (buying goods that never ship), impostor bank calls claiming "fraud protection" transfers, accidental overpayment refund requests, romance and dating app pre-meeting transfers, rental deposit scams, prize and giveaway claim fees, and the "send a test payment" trick used by job recruitment scammers.

Can Truvizy detect Zelle and Venmo payment scams?

Truvizy's AI-powered analysis at truvizy.app scans suspicious links, screenshots, profiles, and videos that scammers use to set up payment app fraud, including fake bank alert texts, fraudulent rental listings, romance scammer profiles, and impostor support call recordings. Submit any suspicious content before sending money to verify whether you are dealing with a known fraud pattern.

Is Zelle or Venmo safer to use?

Neither is "safe" for transactions with strangers. Both treat authorized transfers as final and reversible only at the receiver's discretion. Venmo offers Purchase Protection on payments tagged as "goods or services" for a 1.9% fee, which gives you some recourse. Zelle has no equivalent feature. For any purchase from someone you do not know personally, use a credit card with chargeback rights instead.